Value Investing: Then and Now

Value investing remains relevant by evolving into a disciplined approach that integrates traditional principles with a focus on sustainable growth and industry expertise.

I've been reflecting on the recent commentary regarding the performance of value stocks from several prominent figures in value investing. Some have suggested that the era of value investing has come to an end and that it's time to embrace a different investment framework. However, I strongly disagree with this notion.

Aswath Damodaran has pointed out that proponents of value investing can be dogmatic and fundamentalist, adhering strictly to tradition or rituals. While I respect his perspective, I do not share this view based on my own experiences with the framework. Investing, from my perspective, is both an art and a science; neglecting either aspect can render the approach ineffective.

So, what is truly happening with value investing?

Over the past decade, value stocks underperformed compared to growth stocks and the broader market. The Morningstar US Value Index returned 134.05%, while the Morningstar US Growth had a remarkable return of 237.74%.

After reading on several analyses of the market, there are a few reasons why this has happened:

1. Tech Dominance: The spectacular rise of technology stocks, which make up a much larger portion of growth indices (63%) compared to value indices (13%), has contributed to the outperformance of growth stocks.

2. Low Interest Rates: Historically low interest rates have favored fast-growing companies that rely on debt to finance capital investments and research and development.

3. Sector-Specific Issues: In 2023, the regional banking crisis negatively impacted financial stocks, which are a significant component of the value category.

The one-million-dollar question is: Does value still hold the hope of providing a better return?

To answer this question, I’d like to bring your attention to the figure below, Bruce Greenwald.

Bruce is an American economist and a professor at Columbia Business School. He has earned a reputation as a leading authority on value investing, with The New York Times referring to him as "a guru to Wall Street's gurus." Greenwald's book, "Value Investing: From Graham to Buffett and Beyond," is considered one of the seminal works on the subject.

")

The book comprehensively explores value investing principles and strategies, bridging the gap between Benjamin Graham's foundational concepts and the modern applications used by investors like Warren Buffett. In it, he discusses the evolution of value investing from Ben Graham's era to Buffett, focusing on concepts such as asset value, earnings power value, and growth value. He also emphasizes identifying and valuing a company's sustainable competitive advantages. The book offers a refreshing perspective on how Ben Graham's views on value, Buffett's approach, and the current realities shaped by the rise of AI stocks intersect.

Before exploring the recent developments in the field of value investing, it is valuable to consider Bruce's insights on its core tenets.

I. Fundamental Principles and the Shift in the Landscape

Value investing, as conceived by Graham, Dodd, and Buffett, consists of two fundamental ideas:

Seeking under-the-radar opportunities: The first principle is to seek out opportunities in places where others are not looking and to avoid the crowded markets that are paying inflated prices for glamorous investments. The idea is to focus on statistically undervalued assets that may appear unattractive or out of fashion. This approach remains relevant today. Value investors typically rely on simple statistical metrics to identify these overlooked opportunities while steering clear of crowded and overpriced options.

Employing a rigorous valuation framework: The second important aspect of value investing lies in the approach to valuations that follows the Graham and Dodd tradition. This method emphasizes clarity and precision, which many average investors often overlook. Value investing goes beyond merely applying a multiple to earnings and concluding that a growing business is worth 40 times its earnings. It involves more than just forecasting quarterly earnings. Value investors set themselves apart by taking a meticulous approach to valuation, striving to gain a deep understanding of the asset being acquired rather than relying on simplistic multiples or superficial earnings projections.

Due to its fundamental principles, the field of value investing has undergone significant changes. Traditionally, value investing concentrated on tangible assets (e.g., net-net strategy) and strong competitive businesses (moats, moats, and moats).

However, this approach has had to adapt to the emergence of franchise businesses, defined by their sustainable competitive advantages, often referred to as "moats."

What has changed since Ben Graham began?

Globalization: Traditional manufacturing-based national markets have globalized, intensifying competition and eroding profit margins. As these markets have globalized, the minimum scale required to operate has decreased, leading to heightened competition and increased ease of entry for new players. Since the 1960s, the long-term trends have demonstrated declining profitability and lower barriers to entry. Consequently, throughout this period, growth returns have often been disappointing. The Nifty 50 did not fall out of favor solely because they were overpriced; rather, they became less favorable due to their high valuations and consistently disappointing returns.

The Shift to Services: The economy has shifted towards services, which often operate in local markets. This localization allows dominant companies to establish stronger competitive advantages and earn higher returns. Service markets are typically local, involving goods that are produced and consumed in the same area. These are small markets that large retailers like Walmart can dominate.

Over time, this has led to increasing barriers to entry for new businesses, higher monopoly profits, and greater perceived value in growth. Additionally, advancements in technology are exacerbating these issues. In the past, companies like IBM handled everything internally, but now the trend is moving towards specialized components, where instead of a single company providing all services, different firms handle specific parts of a service.

Technology's Impact: Technological advancements have further fragmented markets. Companies specializing in niche areas within the technology sector can achieve market dominance and exercise pricing power. Each company holds a small piece of the overall technology landscape.

For example, Google dominates the search engine market, while Microsoft primarily controls operating systems. Adobe focuses on fonts and video processing, Oracle specializes in databases and related applications, and Salesforce is dedicated solely to sales management software.

As technology progresses, these markets have become more distinct, with companies establishing strong positions within them. It's important to remember that smaller markets can be advantageous, as firms that dominate these niches often generate above-average returns. The presence of barriers to entry means that genuine growth potential has become increasingly valuable.

Looking at U.S. profit data from the late 1980s and early 1990s, profits represented approximately 88.5% of national income. Today, that figure has dropped to between 13% and 14%. This shift highlights the emergence of these monopolistic markets and the importance of growth in maintaining profitability. If you're not focused on growth, you risk being left behind.

But the question remains: why has the value approach underperformed? Does it still work?

II. Recent Underperformance of Traditional Value Strategies

Bruce said that the underperformance of traditional value strategies stems from a fundamental shift in the global economy, driven by two major transformations: the transition from agriculture to manufacturing and the subsequent shift from manufacturing to services.

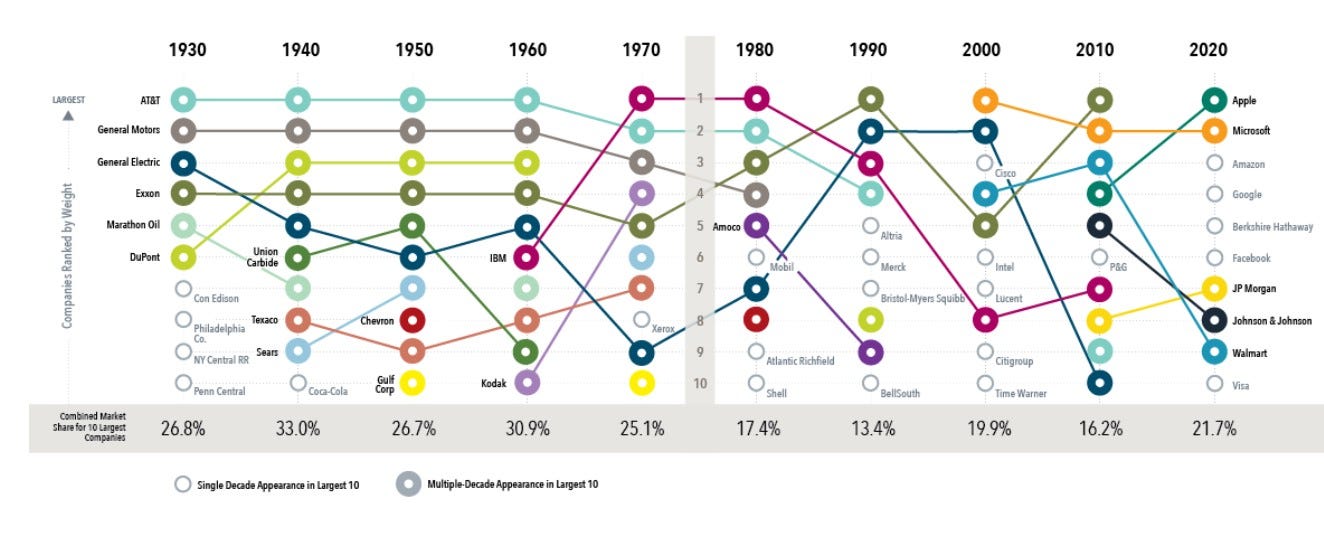

Transformation from Agriculture to Manufacturing: This shift, which largely played out in the decades following World War II, brought about significant productivity growth and the rise of large, dominant manufacturing firms like General Motors, IBM, and DuPont. These companies enjoyed substantial economies of scale and limited competition, making them classic examples of franchise businesses with strong moats.

The old and new kings. Source: awealthofcommonsense.com This era favored traditional value investors who focused on identifying undervalued assets and earnings power, as growth was less crucial in these stable, highly profitable industries.

In our previous article, we discussed earnings power. You can find it linked below.

Transformation from Manufacturing to Services: Starting in the late 1980s and early 1990s, the global economy began transitioning from manufacturing to services. While services initially exhibited slower productivity growth and a less even income distribution compared to manufacturing, this shift also brought about a resurgence of franchise businesses with strong moats. This was due to several factors:

Localization of Service Markets: Service markets tended to be more localized than manufactured goods, which could easily be traded across national borders. This created opportunities for companies to establish dominant positions in smaller, geographically defined markets.

Rise of Technology-Driven Service Businesses: The emergence of companies like Google, Microsoft, and Amazon illustrated how technology could be leveraged to create scalable, dominant service businesses with strong network effects and customer captivity.

Fragmentation of Technology Markets: As technology evolved, it became more specialized and disaggregated. Rather than having a single company like IBM dominating the entire computing landscape, individual companies emerged to specialize in specific areas like search (Google), operating systems (Microsoft), or cloud computing (Amazon). This fragmentation further contributed to the rise of powerful, specialized franchise businesses.

III. Implications for Value Investing

The growing dominance of franchise businesses in the service sector, combined with the rising importance of technology, has significant implications for traditional value investing strategies. Many observers have noted that value investors often appear resistant to the concept of growth; however, growth has become more crucial than ever. So, what do these shifts mean for value investing as an investment method?

Focus on Growth: In this new environment, growth has become a more critical driver of value. Companies with strong moats and the ability to generate sustainable growth can command premium valuations, while traditional value metrics based solely on assets and current earnings may understate their true worth.

Need for Specialization: The complexity of valuing growth companies requires a deeper understanding of specific industries, technologies, and management teams. As Greenwald notes, value investors will increasingly need to specialize in one or a few industries to effectively assess the sustainability of moats and the potential for long-term growth.

Discipline and Conservatism: While recognizing the importance of growth, Greenwald cautions against excessive optimism and emphasizes the need for discipline and conservatism in valuation. The linear nature of his returns-based framework encourages sensitivity analysis and helps investors guard against the behavioral biases often associated with growth investing.

Greenwald does not explicitly address the role of low interest rates in the underperformance of traditional value strategies. However, one could infer that in a low-yield environment, investors might be more inclined to chase growth and pay higher multiples for companies with strong growth prospects, potentially contributing to the outperformance of growth stocks relative to value stocks.

IV. The New Investor in Town: Value-Oriented Growth Investors vs. Ordinary Growth Investors

Greenwald then highlights several key characteristics that set value-oriented growth investors apart from their ordinary growth investor counterparts:

1. Focus on Sustainable Franchises

Value-oriented growth investors prioritize investments in companies with demonstrable and sustainable competitive advantages – what Warren Buffet refers to as "moats." They recognize that growth only creates enduring value when it occurs within the protective boundaries of a strong franchise. They rigorously assess the minimum required scale for new entrants, the stability of market share over time, and the factors contributing to customer captivity, such as habit, search costs, and switching costs.

Ordinary growth investors may be more captivated by the allure of rapid growth without giving sufficient consideration to the durability of the company's competitive position. This can lead to investments in companies whose growth is unsustainable or vulnerable to disruption, ultimately resulting in disappointing returns.

2. Emphasis on Capital Allocation and Management Quality

Value-oriented growth investors place significant emphasis on analyzing management's capital allocation skills and their ability to reinvest earnings effectively. They look for evidence of a consistent track record of value creation through initiatives like acquisitions, cost reduction projects, and operational improvements. They scrutinize expansion strategies to ensure that companies are leveraging their competitive advantages and not venturing into areas where their moats are less effective.

Ordinary growth investors may be less focused on capital allocation, potentially overlooking the risks of poor management decisions that can squander growth opportunities and destroy shareholder value.

3. Disciplined Valuation and Conservative Growth Estimates

Value-oriented growth investors employ a rigorous, returns-based valuation framework that incorporates a margin of safety to account for uncertainties and potential risks. They are disciplined in their growth projections, starting with conservative estimates and recognizing the potential for franchise fade over time. They understand that overly optimistic growth assumptions can lead to inflated valuations and disappointing returns.

Ordinary growth investors may be more susceptible to the "growth trap," overpaying for companies based on overly optimistic growth forecasts. They might also neglect to consider the inevitable erosion of competitive advantages, leading to a false sense of security about the long-term sustainability of growth.

4. Long-Term Perspective and Patience

Value-oriented growth investors take a long-term perspective and are patient in waiting for the right investment opportunities. They recognize that building a sustainable franchise and generating long-term value takes time. They are less concerned with short-term market fluctuations and are willing to hold investments for extended periods, allowing the power of compounding to work in their favor.

Ordinary growth investors may be more focused on short-term performance and may be quicker to sell investments if they don't see immediate results. This short-term mindset can lead to missed opportunities and suboptimal returns.

5. Industry Specialization and Expertise

Value-oriented growth investors understand that effectively assessing growth prospects and the durability of competitive advantages requires deep industry knowledge. They are likely to specialize in one or a few industries where they can develop a nuanced understanding of the competitive landscape, technological trends, and key drivers of value creation.

Ordinary growth investors may take a more generalist approach, investing across a broader range of industries. While diversification can have its merits, it can also lead to a more superficial understanding of individual companies and their growth potential.

In essence, value-oriented growth investors represent a hybrid approach that combines the rigor and discipline of traditional value investing with a sophisticated understanding of growth dynamics. They recognize that growth can be a powerful driver of value, but only when it is sustainable and occurs within a durable competitive advantage. They are disciplined in their valuations, patient, and committed to developing deep industry expertise.

Conclusion

In conclusion, the underperformance of traditional value strategies in recent years reflects a fundamental shift in the global economy, driven by technological advancements, the transition to service-oriented markets, and the rising dominance of franchise businesses with strong moats. However, this does not signify the end of value investing. Instead, it calls for an evolution of the approach. As Bruce Greenwald and other thought leaders suggest, the future of value investing lies in embracing a hybrid model that integrates the discipline and rigor of traditional methods with a nuanced understanding of growth dynamics. By focusing on sustainable competitive advantages, disciplined valuation, and deep industry expertise, value-oriented growth investors can unlock opportunities that traditional value or growth strategies might overlook. This refined approach ensures that value investing remains a relevant and powerful framework, even in an era dominated by rapid technological progress and fragmented markets. Far from being obsolete, value investing continues to thrive when adapted to the realities of today's economy.

Today's quality investors might actually be the real value investors if you think about it.

could you come up with a current example that fits that framework? LVMH, PRYMF, BLD, BLDR or are about what stocks are you talking about?