What Constitutes an Economic Moat?

Michael Mauboussin's insights on economic moats highlight their critical role in sustaining competitive advantages and driving long-term value creation.

In the fast-changing world of investing, there are some ideas that just never go out of style, and one of those is the concept of an economic moat. Warren Buffett brought this idea to the spotlight, and since then, it’s been a key part of how many people approach value investing.

But what exactly constitutes a moat in today's rapidly changing business environment?

Enter Michael Mauboussin, a renowned strategist and author whose insightful analysis breathes new life into this timeless concept.

Mauboussin's exploration of moats isn't just a rehash of old ideas; it's a fresh perspective that challenges us to think deeper about sustainable competitive advantages. In a world where technological disruption can erode traditional barriers overnight, understanding the nuances of modern moats is more crucial than ever.

Are the moats of yesterday still relevant today? How can investors identify and evaluate these protective barriers in an age of digital transformation and global competition?

As we dive into Mauboussin's article (I’ll share the link below), we're not just reading about business strategy; we're uncovering the DNA of successful companies that have managed to keep competitors at bay. His analysis goes beyond the surface, delving into the intricate dynamics that allow some firms to maintain above-average returns over extended periods. It's a masterclass in strategic thinking that every investor, whether novice or seasoned, should pay close attention to.

https://www.morganstanley.com/im/publication/insights/articles/article_measuringthemoat.pdfSo, buckle up as we embark on this journey through the moats of the modern business world!

I. What is a Moat?

I have been reading many definitions of a business moat. While many of them are accurate, they can still be vague and do not clearly define what makes a moat effective.

A moat is a metaphor for the defensive barriers that protect a company from competition and allow it to earn above-average returns on invested capital (ROIC) for extended periods. These barriers can be tangible, such as patents or exclusive access to resources, or intangible, like strong brands or network effects.

II. Why Moats Matter?

Mauboussin emphasizes that a wide and durable moat is essential for long-term value creation. Companies with solid moats are better positioned to withstand competitive pressures, maintain pricing power, and generate consistent profits, ultimately rewarding their shareholders with superior returns.

There are several key factors contributing to a strong moat:

Industry Structure: Mauboussin highlights the importance of analyzing industry dynamics through Porter's Five Forces framework, which considers the threat of new entrants, bargaining power of suppliers and buyers, rivalry among existing competitors, and the threat of substitutes. Favorable industry structures, with high barriers to entry and limited competitive intensity, contribute to wider moats.

Porter’s Five Forces. Source: RAISE Barriers to Entry: We have discussed the importance of Barriers to Entry based on Bruce Greenwald and Judd Kahn's “Competition Demystified.” However, Mauboussin categorizes various barriers that can deter new entrants and protect incumbents.

Economies of scale: Large incumbents can produce goods or services at lower unit costs, making it difficult for smaller entrants to compete on price.

Network effects: The value of a product or service increases as more users join the network, creating a powerful advantage for incumbents with large user bases.

Customer switching costs: High costs associated with switching to a competitor, such as contract penalties or the need to retrain employees, can deter customers from leaving established providers.

Intangible assets: Strong brands, patents, and proprietary technology can give incumbents a significant edge over rivals.

Value Creation: The paper introduces the concept of the "value stick" (which we touched a bit in JC Penney’s article), which illustrates how companies can create value by either increasing willingness to pay (WTP) or lowering willingness to sell (WTS).

Increasing WTP: Companies can differentiate themselves and command higher prices by offering superior products, building strong brands, leveraging network effects, or reducing search costs for customers.

Lowering WTS: Companies can enhance their cost leadership by lowering supplier costs through data sharing, improving productivity, accessing unique inputs, managing their balance sheets effectively, or fostering a positive employee culture that lowers the opportunity cost for employees.

I previously wrote an article about the value stick, which you can find here. In 2019, JC Penney's decision to shift to an everyday low-pricing strategy backfired spectacularly, demonstrating the dangers of misunderstanding customer value perception. By eliminating sales and coupons, the company inadvertently removed the "thrill of the hunt," which its core customers deeply valued.

This misstep can be analyzed using a value-based pricing strategy. The value stick model illustrates how JCPenney's new approach compressed its profit margins by narrowing the gap between customers' "willingness to pay" and the actual price point. JCPenney failed to recognize that the bargain-hunting experience was an intangible yet crucial element of the overall value proposition for many customers. You can check the article below.

III. Measuring Value Creation

Mauboussin describes the relationship between return on invested capital (ROIC) and the weighted average cost of capital (WACC) as a measure of value creation.

ROIC, calculated as net operating profit after taxes (NOPAT) divided by invested capital, represents a company's profitability relative to the capital invested in its operations. It reflects how effectively a company utilizes its resources to generate profits.

WACC represents the average cost a company pays for its financing, taking into account the proportion of debt and equity in its capital structure. It reflects the minimum return a company needs to earn to satisfy its investors.

The spread between ROIC and WACC is crucial for evaluating a company's value-creation potential.

If ROIC exceeds WACC, the company generates returns that surpass its cost of capital, indicating it is creating value for its shareholders.

Conversely, if ROIC is lower than WACC, the company is destroying value as it fails to earn enough to cover its financing costs.

Mauboussin illustrates this concept with the analogy of acquiring two identical cash flow streams, one yielding 5% and the other 7%. Investing in the 5%-yielding stream would result in a failure to earn the opportunity cost of capital, as the 7%-yielding alternative exists.

It sounds simple to me when I first read this, but in reality, it is much more complex than finding the cheapest source of funds and reinvesting in high-return projects because it is also about consistency. A business can provide shareholder returns in one year and burn the gains the next year by investing in a failed project (e.g., Apple Vision Pro).

He then emphasizes that while a positive ROIC is desirable, it's not sufficient for sustainable value creation. Companies must earn returns above their WACC and sustain this positive spread over time. This requires consistently identifying and investing in attractive opportunities, highlighting the importance of strategic decision-making and a company's ability to maintain its competitive advantage or "moat.”

IV. Strategies for Value Creation

Mauboussin explains that companies can create value by either increasing willingness to pay (WTP) or lowering willingness to sell (WTS). These two approaches generally align with differentiation and cost leadership strategies, respectively.

Differentiation Strategy

A firm pursuing a differentiation strategy aims to create products or services that are perceived as unique and superior to those of competitors. The goal is to increase WTP, allowing the firm to charge premium prices. This strategy often focuses on the demand side of the value stick.

He highlights several ways companies can achieve differentiation:

Network Effects: Creating a platform where the value increases as more users join. For example, social media platforms or online marketplaces benefit from network effects.

Complementary Products: Offering products or services that enhance the value of the focal offering. For instance, a smartphone manufacturer might offer a suite of apps and services.

Brand Prestige: Cultivating a brand image associated with high quality, exclusivity, or social status. Luxury goods companies often leverage brand prestige.

Reducing Search Costs: Making it easier for customers to find and evaluate products or services. For example, online retailers offering comprehensive product information and reviews can reduce customer search costs.

Habit Formation: Encouraging repeat purchases by creating products or services that customers become accustomed to using. Subscription services or products with strong brand loyalty can benefit from habit formation.

Switching Costs: Making it costly or inconvenient for customers to switch to a competitor. Software companies with proprietary systems or companies offering personalized services can create switching costs.

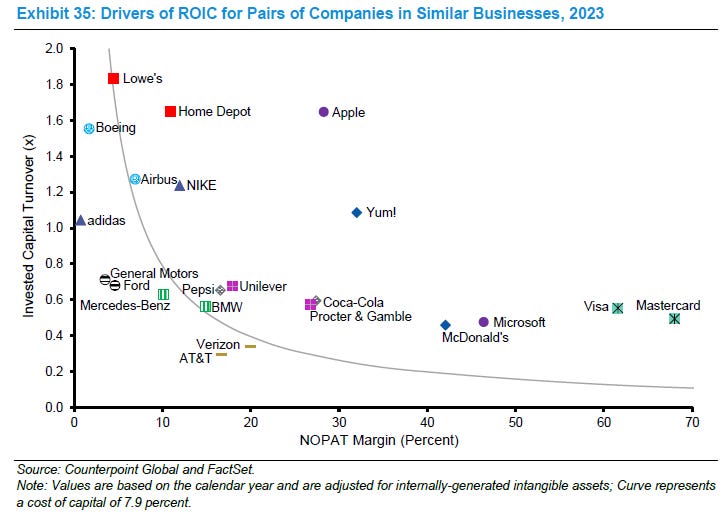

Companies pursuing differentiation strategies tend to exhibit high NOPAT margins and acceptable invested capital turnover. This reflects their ability to command premium prices while maintaining reasonable efficiency in asset utilization.

Cost Leadership Strategy

A firm employing a cost leadership strategy focuses on lowering WTS by producing goods or services at a lower cost than competitors. This strategy often emphasizes the supply side of the value stick. While this strategy may not lead to premium prices, it allows the firm to be more profitable at a given price point.

He outlines various ways to achieve cost leadership:

Economies of Scale: Reducing per-unit costs by increasing production volume. Large manufacturing firms or companies with significant fixed costs often benefit from economies of scale.

Process Innovation: Developing more efficient production processes. Companies investing in automation or lean manufacturing techniques can lower production costs.

Unique Inputs: Accessing raw materials or other inputs at a lower cost than competitors. A company might have exclusive rights to a natural resource or benefit from favorable supplier relationships.

Productivity Advantages: Operating more efficiently than competitors, using fewer inputs to generate the same output. This can be achieved through superior management practices, technology implementation, or employee training.

Learning Curve Effects: Reducing costs through experience and accumulated knowledge. Companies in industries with complex production processes can benefit from learning curve effects as they gain expertise over time.

Firms pursuing cost leadership typically have acceptable NOPAT margins and high invested capital turnover. This reflects their focus on efficient asset utilization and achieving high sales volume relative to their invested capital.

Choosing the Right Strategy

He emphasizes that the most appropriate strategy depends on the specific industry, market conditions, and company capabilities. While both differentiation and cost leadership can lead to sustainable value creation, some research suggests that differentiation is more commonly associated with outstanding long-term results.

Mauboussin also stresses that a company can achieve both differentiation and cost leadership advantages, though this is relatively rare. With its dominant search engine and advertising platform, companies like Alphabet illustrate how network effects can create demand-side and supply-side scale advantages.

Ultimately, the choice of strategy should be aligned with the company's value proposition and its ability to establish a sustainable competitive advantage, or "moat," that protects its profitability from competitors.

V. Conclusion

Measuring a company's moat is crucial in assessing its long-term value-creation potential. By understanding the key factors contributing to sustainable competitive advantage, investors can identify businesses with durable moats and the ability to generate superior returns over time. Remember, investing is not just about picking stocks; it's about understanding the underlying businesses and their ability to create lasting value.

This image made me remember that some timea back I was also thinking to write on Moats🤣😋

Often people skip WACC and look only at ROIC