Unmasking Value Traps

Kodak appeared cheap based on traditional valuation metrics but failed to adapt to the digital revolution, clinging to its legacy film business while underestimating the speed of technological change.

"It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” - Warren Buffett

The importance of spotting these traps can't be overstated. Throughout my career, I've seen countless investors, both novice and experienced, fall into these pitfalls. When you invest in a value trap, you're not just risking short-term losses. You're potentially tying up your capital in an underperforming asset for years, missing out on better opportunities elsewhere. It's like planting your seeds in infertile soil - no matter how long you wait, they're not going to grow.

Now, what causes these value traps? It's rarely just one factor. Usually, it's a perfect storm of issues that create this deceptive situation. Let me break it down for you:

First, you've got companies in declining industries. I remember back in the day when Kodak seemed like a bargain.

Low P/E ratio, strong brand recognition - it looked great on paper. But we all know how that story ended. The digital revolution completely upended their business model, and those who saw it as a value play got burned.

Then there's the issue of financial engineering. Some companies become adept at making their books look good, even when the underlying business is struggling (case in point: Enron).

They might use aggressive accounting practices or one-time gains to boost their numbers. As a seasoned advisor, I've learned to look beyond the headline figures and dig into the footnotes of financial statements.

Management quality is another big factor. I've seen companies with great products and strong market positions falter because of poor leadership. Maybe the CEO is more interested in empire-building than creating shareholder value, or perhaps the board is asleep at the wheel. These issues can take years to play out, all while the stock looks "cheap" based on traditional metrics.

Debt is another red flag I always watch for. Companies with heavy debt loads might seem like bargains, especially in low-interest environments. But when the tide turns - and it always does eventually - these firms can find themselves in deep trouble.

Lastly, there's the psychological aspect. As humans, we're wired to look for patterns and believe in reversion to the mean. We see a stock that's fallen 50% and think, "Surely it can't go lower." But in my experience, there's no floor to how low a stock can go if the underlying business is broken.

Identifying these traps isn't always easy, even for professionals. It requires a combination of quantitative analysis, industry knowledge, and often, a bit of gut feeling that comes from years of experience. However, learning to spot these pitfalls is one of the most valuable skills any investor can develop.

So, to summarize my points, there are six key steps to identify value traps:

Profit consistency: Look for consistent profits over multiple years and the quality of earnings

Industry comparison: Compare the company's performance to its sector and competitors

Future planning: Assess the company's strategy for future growth and product development

Management quality: Evaluate the competence and alignment of the company's leadership

Financial health: Analyze the company's balance sheet and cash flow for signs of deterioration

Competitive position: Analyze the company’s competitive moat

While this list might not be exhaustive, it could help us get a better sense of whether we are seeing a value trap company.

Let’s take this list for a ride!

The company we will analyze is Eastman Kodak (KODK).

1. Profit Consistency:

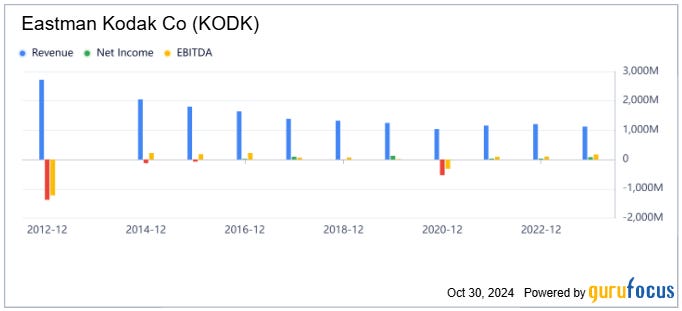

Kodak's profit consistency has been problematic. After emerging from bankruptcy in 2013, the company has struggled to maintain consistent profitability. In recent years, Kodak has shown some improvement, with a net income of $986.2 million in FY2023. However, this follows a significant dip to $111.5 million in FY2022, and the company's historical performance has been volatile. This inconsistency is a red flag that suggests Kodak might be a value trap.

2. Industry Comparison:

Compared to its peers in the imaging and printing technologies sector, Kodak's performance has been subpar. While companies like Canon and Fujifilm have successfully diversified and adapted to the digital age, Kodak has struggled to find its footing. Kodak's P/E ratio of 8.82 might appear attractive, but it's important to note that this is based on a single year of improved performance. The company's gross margin of 17% in Q4 2023 is lower than many of its competitors, indicating potential challenges in maintaining probability.

While Kodak managed to achieve a positive net income in 2023, its profit margin is lower than most of its competitors. HP, Canon, and Fujifilm show stronger profitability. In addition, The revenue difference between Kodak and its competitors is substantial. HP's revenue is over 45 times that of Kodak, while even the closest competitor in this list, Xerox, has revenue about 6 times higher than Kodak's.

3. Future Planning:

Kodak has made efforts to pivot its business model, focusing on digital printing, packaging, and advanced materials. The company has outlined strategic initiatives, including unifying its Merchant Solutions business globally and prioritizing SMBs. However, these plans are yet to demonstrate consistent results, and the company faces significant challenges in highly competitive markets. The lack of a clear, successful growth strategy is concerning and suggests potential value trap characteristics.

Despite these challenges, Kodak continues to innovate in traditional printing, recently releasing products such as the PRINERGY software and SONORA XTRA next-generation plates, which enhance its product portfolio. Nevertheless, the Print segment has performed poorly, with a decrease in print revenues of approximately $110 million. This decline mostly stems from reduced volumes in Prepress Solutions consumables, equipment, and service, which dropped by $105 million, $10 million, and $4 million, respectively. Additionally, there were volume declines in Electrophotographic Printing Solutions, with consumables and service decreasing by $12 million and equipment by $7 million.

These performance trends raise questions about the management's decision to continue launching new products.

4. Management Quality:

Kodak has experienced several leadership changes since its bankruptcy, which can be a sign of instability. The current CEO, Jim Continenza, has been in his role since 2019. While he has made efforts to turn the company around, the results have been mixed. The management team's ability to execute a successful turnaround strategy remains uncertain, which is another potential red flag for value trap identification.

5. Financial Health:

Kodak's financial health has improved since its bankruptcy, but challenges remain. The company reported a cash balance of $255 million at the end of 2023, an improvement from the previous year. However, Kodak still carries a significant debt load, which could limit its flexibility and ability to invest in growth opportunities. The company's debt-to-equity ratio and other financial metrics should be closely monitored for signs of deterioration.

6. Competitive Position:

Kodak's competitive position has weakened significantly over the past decades. Once a leader in the photography industry, the company failed to adapt to the digital revolution and lost substantial market share. While Kodak has attempted to reposition itself in various imaging and printing technologies, it faces stiff competition from well-established players and innovative startups. The company's ability to maintain or improve its market position in its current focus areas remains uncertain.

Conclusion:

Based on this analysis, Kodak exhibits several characteristics of a potential value trap:

Inconsistent profitability

Underperformance compared to industry peers

Uncertain future growth prospects

Historical management challenges

Ongoing financial concerns

Weakened competitive position

While Kodak's stock may appear cheap based on certain metrics, the underlying fundamentals suggest caution. The company's efforts to reinvent itself are yet to show consistent results, and it faces significant challenges in highly competitive markets. Investors should be wary of viewing Kodak as a straightforward value opportunity and should carefully consider the risks associated with the company's ongoing turnaround efforts.

As with any potential value trap, thorough due diligence and a clear understanding of the company's future prospects are essential before making an investment decision.